If you look solely at order volume this January, the retail economy looks robust. Warehouses are busy, parcels are moving, and consumers are clicking buy.

But if you look at the underlying data, a different, more fragile story emerges.

Our platform has detected a sharp divergence in Q1 fundamentals: Order counts are climbing, but Order Value is down, while GMV continues to accelerate.

We call this the “Empty Calorie” economy

2026 retail trends show the market is consuming more units, but those units are providing less nutritional value to the bottom line. For strategists and investors, this decoupling of volume from value is the first critical signal of 2026. Here is what is happening, and why the old playbook for fulfillment is about to break.

2026 retail trends: the great January ‘flush’

Data from the Deposco supply chain platform shows that retailers started the year sitting on a mountain of unsold goods because inventory levels spiked to 3x normal levels in early January. While this seasonal increase is common, the magnitude of the increase is larger than we’ve seen in previous years.

- What happened: Stores over-ordered after the holiday season and brands loaded up 3PLs expecting a post-holiday boom that didn’t happen at full price.

- The Result: Panic selling. To clear that inventory glut, brands slashed prices. Our data shows those inventory levels have finally crashed back down this week, meaning the “Everything Must Go” sales worked, but at a potentially heavy cost to retailer profit margins.

We are ‘down-trading’ en masse

Here is the weird part: Order counts are up, but the average shopping cart is down while GMV is up year over year and accelerating.

Translation: We are bargain hunting aggressively. Instead of buying one $100 jacket, consumers are buying three $20 items on clearance. We are filling our carts with essentials and lower-tier private labels rather than premium brands. We are buying more things, and the economy is growing, but due to higher volume, lower value items that will impact shippers not looking at the macro trends.

The ‘shipping squeeze’ is coming for your free delivery

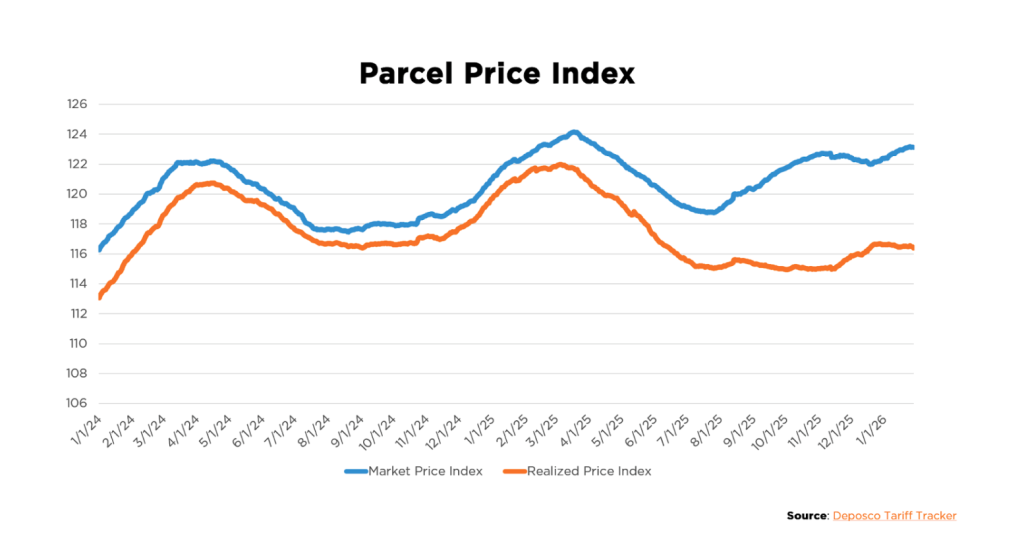

This is where the math gets ugly for businesses. Our Parcel Price Index shows that shipping rates (the cost to move a box) are rising sharply, climbing much faster than the value of the orders being shipped.

Why? Because of a massive inflation gap.

The inflation gap

Under normal conditions, this would just be a margin squeeze. But we are facing a structural anomaly in the logistics market that turns this squeeze into a trap.

Our Parcel Price Index reveals a stark reality: The cost to deliver a box has completely decoupled from broader economic inflation.

- General Inflation (CPI): ~2.7%

- Effective Logistics Cost Increase: ~10-12% (factoring in 2026 GRIs and new residential surcharges). The floor has risen for shippers.

This is the pincer movement creating risk in Q1: Retailers are shipping lower-value baskets into a logistics network that has become more expensive.

However, our Commerce Intelligence data reveals a critical bifurcation in performance. The “Market Price” (Blue Line) reflects the inflation reality for the average shipper. But look closely at the “Realized Price” (Orange Line), it is trading consistently lower.

However, our Commerce Intelligence data reveals a critical bifurcation in performance. The “Market Price” (Blue Line) reflects the inflation reality for the average shipper. But look closely at the “Realized Price” (Orange Line), it is trading consistently lower.

This delta represents the value generated by intelligent fulfillment. Retailers utilizing automated Rate Shopping and dynamic Order Consolidation are successfully insulating their P&L from the full force of carrier hikes. By combining orders and arbitraging carrier rates in real-time, these operators are protecting unit economics even as the broader market faces double-digit cost inflation.

The strategic pivot: 3 market predictions

The “Growth at All Costs” era is officially over. In this environment, the only metric that matters is Quality of Revenue. Based on these data signals, here is how we expect the market to correct in the coming months:

The end of the “Free Shipping” subsidy

The math no longer supports the $35 free shipping threshold. With logistics inflation outpacing basket value by 4x, retailers are effectively subsidizing the consumer’s down-trading behavior. Expect a swift market correction where Free Shipping becomes a premium privilege (thresholds rising to $75+), forcing consumers to consolidate orders.

Agility over availability

The massive inventory spike and flush cycle we just witnessed was a capital-intensive error. The winners of 2026 won’t be the brands with the most stock; they will be the brands with the fastest Inventory-to-Cash cycle times. We expect a strategic pivot toward leaner, demand-driven allocation rather than bulk forward-stocking.

The rise of hard bundling

To fight the Parcel Price Index, product strategy must change. Retailers will increasingly remove the option to buy single, low-margin units. Virtual Bundling and forcing a minimum viable basket size will move from a marketing tactic to a financial necessity to protect unit economics.

The takeaway

Volume is vanity; margin is sanity. The data suggests that 2026 will be the year retail stops chasing the number of orders and starts obsessing over the profitability of the box.

For more information on how Commerce Intelligence will shape 2026, schedule your free strategy session today.